What Does Switzerland Export To The US? A Detailed Guide

Switzerland plays a vital role in U.S. trade, supplying a wide range of high-value and specialized products. From pharmaceuticals and

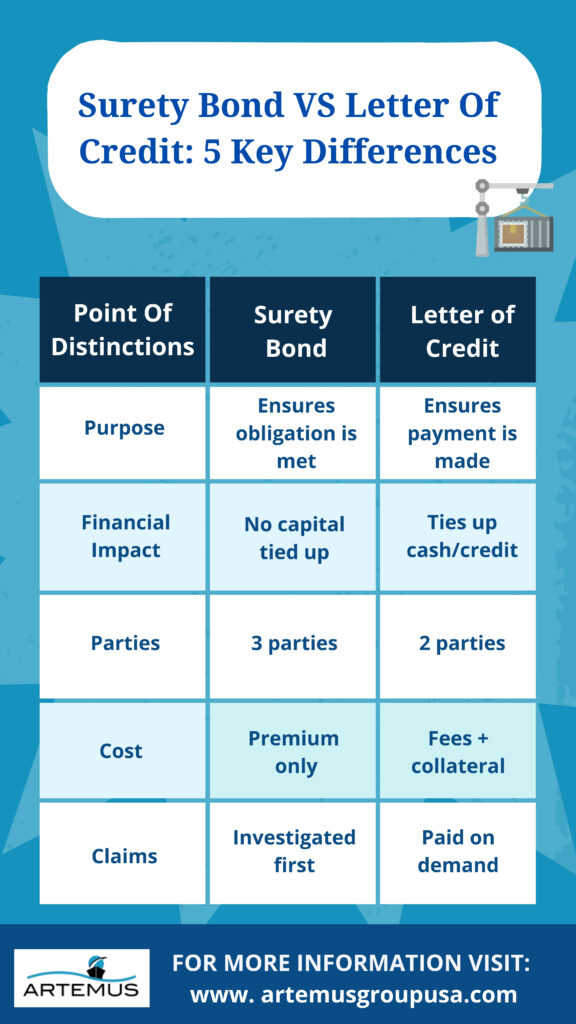

When dealing with international trade and financial transactions, businesses often rely on financial instruments to guarantee obligations. Two of the most common options are Surety Bonds and Letters of Credit (LCs). While both serve as financial guarantees, they differ significantly in terms of cost, risk, and usage. Understanding these differences is crucial for businesses involved in global trade, shipping, and customs compliance.

For companies navigating the complexities of U.S. import regulations, compliance is equally critical. Artemus provides ISF filing software, AMS filing software, & AES filing software, ensuring smooth and hassle-free customs filings for shipments entering and exiting the U.S. Whether securing financial guarantees or streamlining regulatory requirements, businesses must choose the right tools for operational efficiency.

In this article, we’ll break down the key differences between Surety Bonds and Letters of Credit to help you make informed decisions for your business.

Table Of Contents

A surety bond is a financial agreement that guarantees the fulfillment of an obligation or commitment.

If the principal fails to meet the agreed-upon obligation, the surety compensates the obligee and later seeks reimbursement from the principal.

A Letter of Credit (LC) is a financial instrument issued by a bank that guarantees a buyer’s payment to a seller, ensuring that transactions, especially in international trade, proceed smoothly. It acts as a promise from the bank that the seller will receive payment as long as they meet the terms and conditions specified in the LC.

Related: Export Documentation Requirements To Export From The USA

When businesses need to provide financial guarantees, they often choose between a Surety Bond and a Letter of Credit (LC). While both serve as risk management tools, they operate differently and have distinct financial implications. Understanding their key differences can help you make an informed decision.

Related: Ocean Freight Documentation For Imports: A Crucial Checklist

Surety bonds are designed to protect everyone involved. The surety company evaluates the contractor’s history, financial strength, and capabilities before issuing a bond—acting as a second set of eyes to ensure the contractor is fit for the job. This prequalification process alone offers peace of mind to project owners.

Moreover, the bond’s structure encourages resolution before payout. This reduces misuse and shields contractors from automatic payouts. Since sureties absorb the initial risk and expect repayment from the contractor if a claim is paid, they’re highly motivated to prevent unnecessary claims.

In contrast, a letter of credit guarantees immediate payment to the project owner, even if the contractor believes the claim is unjust. While this benefits the beneficiary, it can expose the contractor to significant financial losses without recourse.

Related: How To Get Import And Export License In USA: Quick Overview

When evaluating financial instruments to guarantee contractual obligations, businesses often consider Surety Bonds and Letters of Credit (LCs). Opting for a surety bond over an LC can offer several advantages that enhance financial flexibility and operational efficiency.

Surety bonds do not encumber a company’s credit capacity, allowing businesses to maintain their existing credit lines for other operational needs. In contrast, LCs often require collateralization, tying up cash or credit and potentially restricting liquidity.

In the event of a claim, surety providers conduct thorough investigations to validate the claim’s legitimacy, offering the principal an opportunity to address disputes before any payout. Conversely, LCs are demand instruments that can be drawn upon by the beneficiary without prior validation of the claim, posing a higher risk of immediate financial impact.

Surety bonds often come with lower costs compared to LCs, which may include various fees such as commitment and utilization fees. Additionally, the surety market is generally perceived as stable, providing reliable financial backing without imposing restrictive covenants that are commonly associated with LCs.

By choosing a surety bond over a letter of credit, businesses can benefit from enhanced financial flexibility, more favorable claim resolution processes, and potentially lower costs, all of which contribute to more efficient and secure operations.

Related: When Is A Customs Bond Required? Situation To Consider

A Letter of Credit (LC) is a financial instrument that guarantees payment between a buyer and a seller, providing security in trade transactions. It is particularly beneficial in international trade, where trust and regulatory differences can create uncertainty. Here’s when an LC is a better option:

If you’re exporting to a new market or dealing with a buyer whose creditworthiness is uncertain, an LC ensures that payment will be made as long as the terms are met.

For significant transactions where a default could cause major financial loss, an LC provides a layer of security by involving the bank as an intermediary.

Different countries have varying trade laws, and currency exchange risks may arise. An LC helps mitigate these risks by guaranteeing payment in an agreed currency.

If you are a buyer dealing with a new supplier and want to ensure they deliver the agreed goods or services before payment, an LC serves as a safeguard.

In cases where open account transactions or advance payments could lead to fraud or non-delivery, an LC assures that goods will be shipped and payment will be honored.

An LC can include performance clauses, ensuring that suppliers adhere to strict delivery timelines, and reducing delays in project execution.

Related: What Happens After Custom Clearance Completed? 9 Next Steps

When deciding between a Surety Bond and a Letter of Credit (LC), it’s essential to understand how each works and which is best suited for your financial and business needs. A Surety Bond is a financial guarantee provided by an insurance company or surety provider, ensuring contractual obligations are met without tying up significant capital.

On the other hand, an LC is a bank-issued financial instrument that guarantees payment, often requiring collateral that may impact liquidity.

A Surety Bond is often the better choice for businesses looking to preserve their credit lines and working capital, as it does not require full collateral upfront. It is widely used in industries like construction, regulatory compliance, and government contracts, where businesses need long-term guarantees.

Conversely, a Letter of Credit is ideal for international trade or high-value transactions where immediate payment security is a priority. It provides assurance that a seller will be paid as long as the contractual conditions are met.

Ultimately, the decision depends on your financial flexibility, industry requirements, and risk tolerance. If maintaining liquidity and cost-effectiveness is a priority, a Surety Bond may be the better option.

However, if guaranteed payment with minimal risk is the goal, especially in global trade, a Letter of Credit could be the right choice. Evaluating your specific needs will help determine the best financial instrument for your situation.

Related: 10 International Shipping Documents To Must Have In 2024

For businesses operating across borders, compliance with U.S. Customs is essential. Artemus Transportation Solutions provides cutting-edge software solutions for:

These softwares ensures smooth customs processing, reduces penalties, and integrates well with your surety bond or LC-backed logistics operations. When working on international contracts, integrating finance and compliance workflows boosts efficiency and accuracy.

A surety bond helps preserve your working capital and includes dispute protection, making it more contractor-friendly.

Yes, federal projects over $150,000 require bonding under the Miller Act. Many state and local projects follow similar rules.

Yes, some contracts may require multiple forms of financial assurance, especially on high-value or international projects.

Not necessarily. LCs require sufficient collateral and a good relationship with your bank. Surety bonds require prequalification but often come with lower upfront cost.

Yes, some complex or high-value projects may require a combination of both, depending on the contractual and jurisdictional requirements.

The surety will investigate the claim. If it is found to be valid, the surety may pay the obligee or complete the obligation — and then seek reimbursement from you, the principal.

Yes, but new or small contractors may need to provide more financial documentation or use small business surety bond programs (like the SBA Surety Bond Guarantee Program).

Generally, no. Surety bond premiums are non-refundable, as the bond remains in force during the coverage period even if no claims are made.

Surety bonds are typically safer for contractors. Unlike letters of credit, they include dispute resolution and claims investigation, preventing wrongful payouts and protecting your business reputation and cash flow.

Surety bonds are generally more affordable, as they require a small premium (usually 1–3% of the bond amount), whereas letters of credit often require 100% collateral and ongoing bank fees.

Understanding the distinction between surety bonds and letters of credit is key to protecting your construction business. While surety bonds offer better financial flexibility and long-term advantages, letters of credit may suit specific high-risk or international scenarios.

Make decisions aligned with your goals and project needs. And for seamless compliance in global trade, Artemus Transportation Solutions provides industry-leading ISF, AMS, and AES software to support contractors, freight forwarders, and import/export professionals.

Switzerland plays a vital role in U.S. trade, supplying a wide range of high-value and specialized products. From pharmaceuticals and

In 2026, the US-Europe trade relationship continues to power global commerce, driven by exports of energy, advanced machinery, and pharmaceuticals

The economic partnership between the United States and Norway is a sophisticated and evolving pillar of transatlantic commerce. U.S. exports